As per Goldman Sachs, the South African Rand is expected to endure larger losses if the U.S. dollar reverses further of its November fall, and it has also identified the British Pound as almost as susceptible for comparable reasons.

As per Goldman Sachs, the South African Rand is expected to endure larger losses if the U.S. dollar reverses further of its November fall, and it has also identified the British Pound as almost as susceptible for comparable reasons.

After the South African Reserve Bank (SARB) lifted the domestic cash rate to its peak point since 2009 on Thursday, the Rand seemed ready to advance against the US Dollar, but by Friday the USD/ZAR pair had surged back over the 17.0 mark.

In a partially turnaround of the hefty losses that drove most U.S. currency rates down during most of November, the USD/ZAR exchange rate rose on Friday as the Dollar rose from multi-month lows versus several currencies.

Kamakshya Trivedi, co-head of Forex strategy at Goldman Sachs, believes that the Dollar’s weakness thus far in November may have been exaggerated in some cases. The Rand, specifically, is one of the sharper instances in which the Rand’s November recognition emerges susceptible to a pullback.

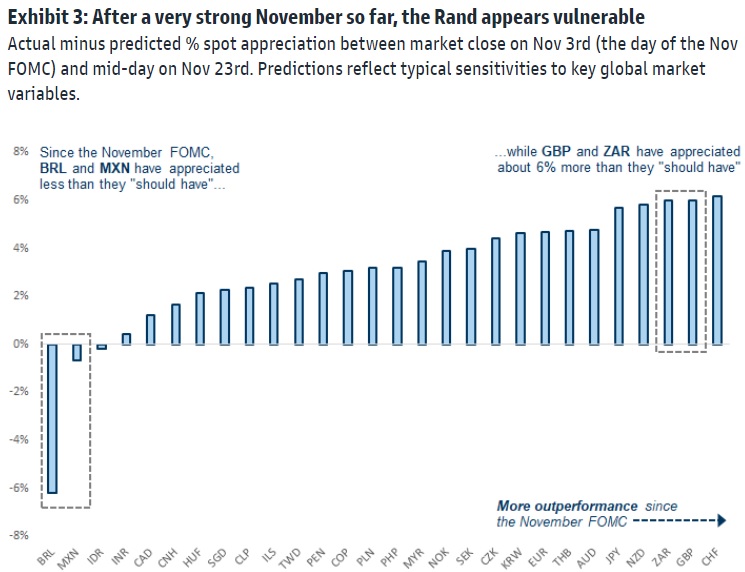

“Exhibit 3 demonstrates that, along with GBP, the lightly-positioned Rand has gained around 6% more against the Dollar than it ‘should have’ since the November FOMC meeting depending on its normal sensitivity to major global market determinants,” he says in a study briefing published on Wednesday.

While the Rand dropped significantly on Friday, it managed to remain the third best performing G20 currency for the month of November, a testament to the magnitude of gains recorded earlier in November when financial and economic conditions converged to push Dollar exchange rates down.

As investors and speculators recorded profits on several of the most actively purchased and sold deals of the year, the Rand rose from near the bottom of the G20 league standings for the entire year to inside the top quartile.

“Not all of the Rand’s recent rise can be explained by positioning or the broad Dollar: the Rand is one of the currencies most susceptible to optimism around a Chinese reopening, for instance,” adds Trivedi.

Goldman Sachs ascribes a significant portion of November’s exceptional performance to South Africa’s trade ties with China and the Rand’s responsiveness to fluctuations in the Renminbi, which means that the Rand could profit further from any event that enhances the economic prospects for China in the near future.

Nonetheless, and on the negative side, Trivedi has cautioned that local economic data poses a risk to the Rand, particularly the discharge of the South African current account balance estimate on December 8, while Goldman Sachs forecasts a revival in U.S. Dollar exchange rates through the end of the 2022.

“There is a significant possibility that the Rand’s November strength might retreat compared to other currencies with equally high ‘beta’ values. Specifically, we will keep looking for more information on the policy response in Brazil so that we can re-engage our position to be long BRL vs ZAR “Trivedi and coworkers claim.

Dollars were sold substantially from the beginning of this month, but especially when official data was published on November 10 indicating that U.S. inflation rates fell more than anticipated in October, data that was provided amid rumors of a probable change in China’s coronavirus containment strategy.

While containment measures have since been strengthened in portions of China, the rumors were a blow to global economic optimism, which weighed severely on the Dollar amidst market attention on the possibility of the Federal Reserve (Fed) raising interest rates in the future at a slower pace.

Nevertheless, this emphasis may have been misguided, to the potential advantage of the dollar and the harm of the rand, since there is a danger that the Federal Reserve would raise its interest rate higher and for a longer period of time than financial markets now anticipate.

In anticipation of the Personal Consumption Expenditures inflation data and the non-farm payrolls data expected out on Thursday and Friday, the market will probably pay close attention to Fed Chairman Jerome Powell’s previously unplanned address on next Wednesday.

A few days back, Trivedi’s teammates remarked, “We believe markets and the FOMC will begin to reverse course on the large FCI [financial conditions index] softening over the previous month, which we believe is still incompatible with the Fed’s policy objectives.”