A totally unexpected charge of £700 million related to mis-selling of payment protection insurance (PPI) and a loss from the sale of African business caused the London-based Barclays Plc (NYSE: BCS) to swing to a loss in the fiscal 2017 second-quarter, from a net profit in the similar period last year.

The quarterly revenue also fell short of expectations. However, the bank surpassed adjusted pre-tax profit expectations of analysts.

Additionally, the bank has completed its restructuring and the business has been simplified as explained below.

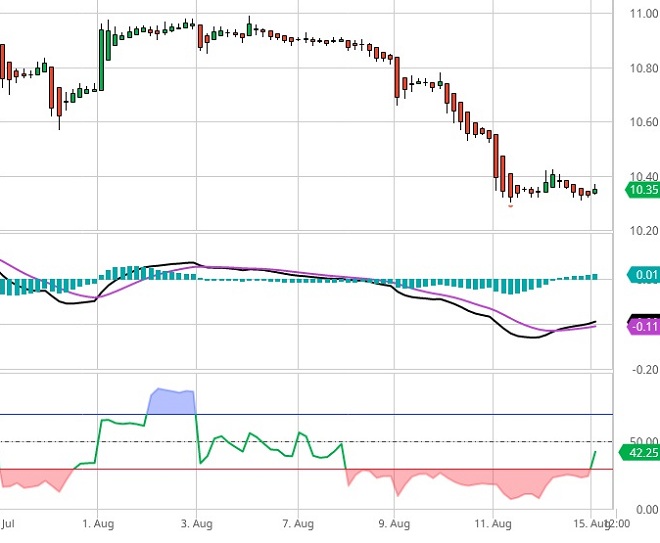

Thus, we forecast a short-term recovery in the share price, which closed at $10.05 on Friday.

The banking and finance company reported revenues of £5.06 billion in the quarter ended June 2017, down from £5.97 billion in the corresponding quarter a year ago. In Q2 2017, the net loss attributable to Barclays was £1.40 billion, compared with a net profit of £677 million in Q2 2016.

Barclays UK

During the quarter, Barclays sold 33% of its Africa unit at a loss of £1.4 billion. Additionally, the bank also took a £1.1 billion impairment charge related to the African business stake sale. With this sale, Barclays has brought its stake in African business to 15%, from 62.3% earlier. The stake sale has freed up capital, which was otherwise locked-up to comply with regulatory requirements.

Excluding one-time costs, Barclays recorded adjusted pretax profit of £1.4 billion and exceeded analysts expectation of £1.2 billion.

Equity trading revenues jumped 12% in Q2 2017. However, fixed income trading revenues declined 14.6% on y-o-y basis. Banking revenues remained flat from last year.

The British bank also took a £700 million charge related to PPI (Payment Protection Insurance), a complex investment vehicle sold for more than two decades to customers taking different kinds of loans (mortgages, credit cards, etc.). The UK regulators determined that PPI was not appropriate for all the customers and ordered Barclays and several other banks to pay compensation to the clients. At the end of the June quarter, Barclays had set aside £9.1 billion to cover the cost of PPI compensation.

The stake sale was the final step in the restructuring process, which involved shedding nearly 60,000 jobs and selling several big assets. In June, the bank winded down its non-core business after offloading most of the £400 billion toxic assets assigned to it three years ago.

The bank ended the second-quarter with a CET1 ratio of 13.1%. Return on tangible equity plunged to a negative 4.6% in the recent quarter. Barclays clarified that its core business achieved a return of 7.2%. The bank is now focusing on only two markets, the US and UK. Even though the bank faces several litigations, still, most of the issues related to its operation have been resolved. Thus, fundamentally, the stock is expected to move up higher in the short-term.

Technically, a bullish reversal is indicated by the MACD indicator whose mainline has crossed above the signal line. The RSI indicator is also emerging out of the oversold region. Thus, we can expect an uptrend in the stock of Barclays.

To gain from the uptrend, we shall purchase a high or above option valid until August 29th. The option would be bought when the stock of Barclays trades near 10.30 in the equity market.

The Canadian Dollar demonstrated strength against the US Dollar and the British Pound on Friday,…

The U.S. Dollar has gained strength amid a downturn in global equity markets, a situation…

The Euro to Dollar exchange rate recently reached a new five-week high of 1.09, recovering…

Following the Labour Party's substantial election win, the Pound Sterling has shown resilience, with experts…

As the weekend approached, the British Pound gained strength, bolstered by the news that the…

Pound Sterling is forecasted to weaken against the US Dollar to levels not seen since…

{kind=link}