On Thursday, the Japanese Yen surged against all other currencies after allegations that the administration in Tokyo had interfered in the Forex market to halt losses in a currency that had been subjected to attack from speculative traders for the majority of this year. Japan’s Yen fell to a fresh millennium low on Thursday as the Bank of Japan (BoJ) opted to maintain its long-standing stimulus measures and as the Dollar rose after the Federal Reserve’s September benchmark interest rate announcement and outlook report (Fed).

On Thursday, the Japanese Yen surged against all other currencies after allegations that the administration in Tokyo had interfered in the Forex market to halt losses in a currency that had been subjected to attack from speculative traders for the majority of this year. Japan’s Yen fell to a fresh millennium low on Thursday as the Bank of Japan (BoJ) opted to maintain its long-standing stimulus measures and as the Dollar rose after the Federal Reserve’s September benchmark interest rate announcement and outlook report (Fed).

Nonetheless, the rapid surge in USD/JPY was completely erased during European morning trade and about the time when deputy finance minister for foreign affairs Masato Kanda reportedly informed news agencies that the state had entered the market.

Jonas Goltermann, a senior markets economist at Capital Economics, stated ” Today’s ruling basically puts a boundary in place at 145, which, if central bankers follow through with today’s moves, might become at worst a short-term ceiling for the USD/JPY exchange rate.”

The intervention would’ve have required the disposal of assets from a stockpile of official reserves worth at approximately $1.29 trillion by the end of August. It was prompted by a lengthy series of cautions from Japanese public officials aiming to dissuade strong and sudden currency market movements. Though rises were noticed primarily in Japanese exchange rates, several other currencies rose against the Greenback in the aftermath of the data, while the U.S. Dollar Index started to relinquish previous gains made in the aftermath of the Federal Reserve’s policy position in September.

Capital Economics’ Goltermann said on Thursday “In the United States, where inflationary pressures are nearing their apex and the economy is declining, we believe it is doubtful that projected benchmark interest rates will climb much higher. This means that downward pressure on the Japanese yen will begin to subside in the near future: yen intervention may provide sufficient time to prevent the USD/JPY rate from soaring over its current high.”

Earlier, on Thursday, officials at the Bank of Japan agreed to maintain the domestic cash rate at -0.1% and the 10-year government bond yield goal at 0% with a cap of 0.25 percent. For the purpose of enforcing the yield objective, the BoJ has stated that it will continue to purchase whatever quantities of government bonds are required via daily market activities, unless it appears probable that no bids will be filed at such events.

Craig Botham, chief Asia Pacific economist at Pantheon Macroeconomics, said “A rate rise was categorically excluded for the foreseeable term, and the Bank of Japan reaffirmed its resolve to maintain loose monetary policy until inflation rate is consistently above the 2% objective. Inflation reached 3% in August, but was fueled by energy, food, baseline factors, and yen weakening, all of which are considered temporary shocks by the Bank of Japan.”

The choice was made on the BoJ’s belief that the latest spikes in Japan’s inflation rates are projected to be transitory and on the expectation that it may take some time for the bank to attain its 2% inflation goal stably.

Min Joo Kang, a senior economist for South Korea and Japan at ING, said ” The Bank of Japan has stated clearly that it would maintain its super-low monetary policy until the benchmark inflation rate stabilizes at approximately 2%.”

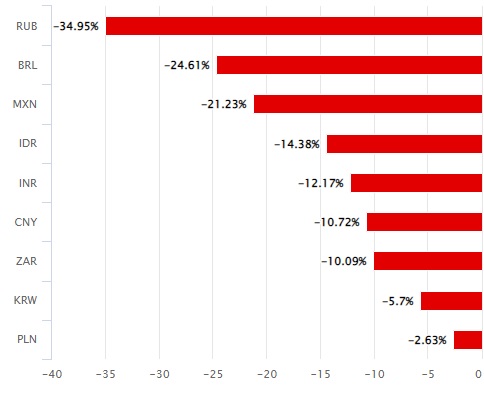

This monetary strategy, nevertheless, has led in increasing interest rate disparities and an added strain for a currency whose value has been substantially dragged down by huge rises in the value of energy imports as a consequence of G7 economic attempts to diversify itself from Russian oil and gas supplies. Yet after Thursday’s interference, the Japanese Yen stood -18.27% down versus the US Dollar this year, and it had also plummeted by double-digit proportions against a bunch of G10 and G20 currencies.

“The yen’s decline in 2022 is neither due to BoJ QE or Fed rate rises. Japan’s surplus in current accounts is insufficient to compensate for its normal 1-2% of GDP value of net FDI [foreign direct investment] outflows, which has contributed to the yen’s weakening this year. This flow gap is unlikely to close until Brent oil falls below $70 “In a recent study presentation, Greg Anderson, global chief of FX strategy at BMO Capital Markets, said the following.